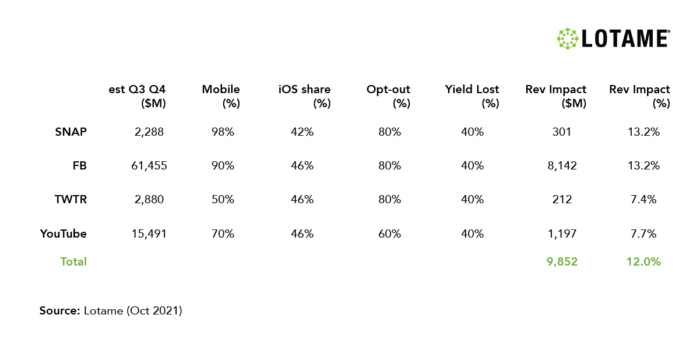

Last fall, Lotame analyzed the possible financial impact of Apple’s initiative to clock advertising IDs on its phone on the top-line revenue for three of the large media / social media players. At the time, we estimated a $9.85 B impact to four companies (Facebook, Twitter, Snap and YouTube), but with over 80% of that impact inuring to Facebook.

Since the fall, a lot has changed, but many of Lotame’s expectations have been borne out. The effects of these changes on these companies are hard to isolate because all four players are still growing extremely strongly, still taking share from the last bastions of traditional media and gaining share in digital media as privacy regulations make it harder and harder for independent publishers and technologies to execute. To add to the complexity, the pandemic has introduced volatile and unpredictable gyrations in the pacing of media spend. With that as context, we said that these changes would have material impact on Facebook and the rest of the industry, but that for the dominant players, the impact would be reflected in reduced future growth, as opposed to any direct setback in top-line sales. This has been largely proven out.

The understanding and analysis of all these moving and countervailing forces is going to increase in importance and complexity in coming quarters because the suppression of IDFAs on Apple phones was only the first domino to fall. Next year it’s expected that Google will finally sunset third-party cookies, affecting monetization on 70% of digital media, and last week the company announced that it expects to also suppress availability of ad IDs on android phones (GAIDs) starting in two years. In addition, both Apple and Google have announced that they plan to make the IP address – a widely used proxy for the identity state – harder and harder to find. All these changes are going to continue to whipsaw the industry, revenue, monetization, winners and losers.

With respect to Facebook itself, our predictions last fall were also largely borne out. We heard from many advertisers, especially small and independent marketers, that they were forced to reduce or eliminate their spend on Facebook because it simply wasn’t effective without the targeting and tracking capabilities inherent in the legacy systems. Facebook validated this on its Q4 earnings call with CFO David Wehner saying “…we believe the impact of iOS overall as a headwind on our business in 2022 is on the order of $10 billion, so it’s a pretty significant headwind for our business. And we’re seeing that impact in a number of verticals. E-commerce was an area where we saw a meaningful slowdown in growth in Q4.”

When you consider the remaining companies in the initial analysis, the impact was expected to be much smaller, and subsequent facts have once again borne that out. Note that both Snap and Twitter are only about 3% as large as Facebook, and both platforms are severely under-monetized relative to their traffic. (While these companies have varying methodologies to estimate users, Facebook has roughly 5 to 6 times the active users of Snap and Twitter and was generating about 30 times as much revenue for most of 2021.) Remarkably, both Snap and Twitter, after years of criticism on monetization, saw revenue bend up sharply last year. Our prediction on impact for Snap in the back half of 2021 was $301 M, and in its earnings call, the company suggested that growth should have been higher in the fourth quarter – 64% instead of 42%, pointing to a $200 M fourth-quarter impact and supporting our estimate of $301 M for the half-year. While Snap complained about the Apple i0S changes, they ultimately shrugged them off and said they were adapting around the issue by enhancing their own native measurement tools, and playing ball with Apple’s native SKAN advertising network tools.

In its fourth-quarter SEC filing, Twitter called the overall impact of Apple’s changes to its revenue “modest” for 2021 (we predicted about 5% of full year), but it also acknowledged that the changes “…will impact our ability to grow our performance advertising business” and suggested these impacts could be durable.

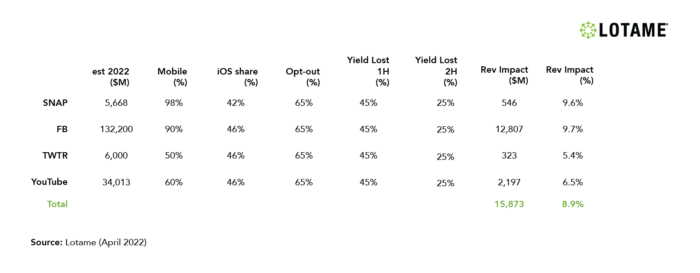

One key issue to consider in predicting the impact of Apple’s App Tracking Transparency (ATT) on large players is how many users block tracking when they download these apps. For our analysis in October 2021, we used 80% across the board. We’ve seen some data come in and as expected, actual results can be all over the map. A weather app might be much more likely to get permission for tracking than a game. Early on AdAge suggested opt-out rates of about 75%. Months later, industry pubs were suggesting opt-out rates between 54% and 62%. A recent analysis from eMarketer landed at 63%. While estimates do vary widely, there does seem to be substantial consensus, supported by observation, that the opt-out rate has improved (i.e., declined) as 2021 progressed. Today, we think a 65% opt-out rate is a better estimate.

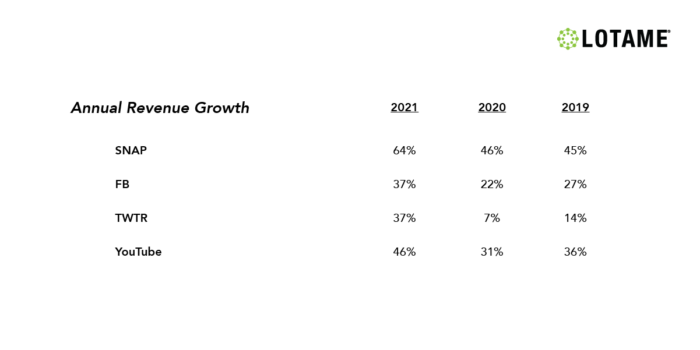

If you consider the analysis from 2021 updated for the current year, again you have to consider the context of giant media companies still experiencing torrid growth. These players were experiencing growth in at least the mid-20’s coming into the pandemic, and they all felt a big hit from it, focused on March, April and May of 2020. As a result, 2021 was a rebound year. Both Facebook and Twitter grew an astounding 37% in 2021. Snap grew 64%.

Looking at next year – we think the IDFA change will have an impact on the companies of nearly $16 B. Again with the lion’s share of that impact (81%) coming from Facebook.

As we have discussed, Snap and Twitter are focused on better monetizing massive user bases and are seeing notable growth. They have largely shrugged off these changes with complaints, but they say they are adapting with new measurement tools and methodologies, and by leveraging Apple’s SKAN network holding their noses. Facebook is doing some of the same if you read their transcripts. They are going to provide new tools, capabilities and native ad tech that will reduce the dependency on Apple. What they’ve realized from this experience is that they are too reliant on the ecosystems of mobile devices while lacking adequate control.

In particular, Facebook is making a major push to drive ecommerce, retail and storefronts to operate entirely in the Facebook system with new tools, capabilities and support. This “walled-garden retrenchment” will be seen elsewhere and reflects Facebook’s realization that it needs to own the marketer from end to end in order to ensure that it can deliver advertising, execution, attribution and measurement for its customers without the business risk of being beholden to the hardware. Facebook too is adapting with new ad tech tools and workaround measurement techniques.

As we move into the back half of 2022, we will no longer be talking about the impact the IDFA changes had on these players – by then 18 months hence. First, we may be moving into a recession. Next, there are other shocks affecting the industry. Third, we’ll be thinking and talking about the next wave of changes and the likely impact on these players (cookies, IP addresses and GAIDs). Finally, the companies themselves will be telling the market that workarounds and adaptations that they have advanced have cauterized the impact on the business.

About the Author

Lotame

Lotame is a global leader in data, identity, and technology, powering smarter, faster, easier digital advertising.